A flight lands early at Teterboro. A board chair needs to be in Midtown for a roadshow. The lead vehicle is confirmed, the backup SUV is on standby, and then someone asks for the certificate of insurance. The document arrives fast, but it raises more questions than answers. The named insured is a different company name than the one on the booking. The auto coverage is listed, but hired and non-owned coverage isn't obvious. There's no clear sign that your company would be protected if a claim pulls everyone into the dispute.

That moment is common for event planners, travel managers, and executive assistants. The transport itself may look polished, but the insurance coverage details often hide in endorsements, footnotes, and missing pages. For executive mobility professionals, that's where risk lives.

This gets harder when bookings cross borders, use affiliate fleets, or involve high-profile passengers. A standard certificate can look complete while still leaving a gap around subcontracted vehicles, priority of coverage, or claims handling. If you're responsible for smooth movement, you need to read insurance like you read an itinerary. You need to know what matters, what's optional, and what's a warning sign.

Introduction

An event planner handling an executive roadshow usually works backward from the visible details. Vehicle class. pickup timing. security preferences. airport coordination. The insurance file often gets checked last, usually because everyone assumes a polished operator has it covered.

That assumption is where trouble starts.

In executive ground transport, the difference between “insured” and “properly insured for this trip” can be the difference between a routine handoff and a day consumed by legal calls. A provider may carry commercial auto insurance, yet the trip might still expose you if an affiliate supplies the vehicle, if your company needs additional insured status, or if one policy applies only after another insurer refuses to pay. Those aren't academic details. They shape who responds first, who pays first, and who gets pulled into the claim.

Practical rule: If the booking involves VIP passengers, affiliate networks, FBO coordination, or multi-city routing, treat insurance review as an operational task, not a filing task.

Many readers get stuck because policy language feels abstract. It doesn't have to. The easiest way to approach insurance coverage details is to think in layers. First, identify the core policies. Next, check the limits. Then verify the endorsements that change how those policies work in real life. Finally, make sure the paperwork matches the operator that's showing up curbside.

Understanding Coverage Foundations

Insurance for executive transport works like airport safety systems. One checkpoint doesn't make a flight safe. You need aircraft maintenance, crew checks, weather review, dispatch controls, and backup procedures. In the same way, one policy doesn't make a chauffeur operation fully protected.

The broader market is moving toward more complex protection needs. The Allianz Global Insurance Report 2026 projects the global insurance market to grow at an annual rate of 5.3% over the next decade, which signals rising demand for more extensive, cross-border coverage. For executive mobility, that fits what planners already see on the ground. More international travel, more connected services, and more pressure to verify details instead of assuming.

Risk transfer in plain language

Insurance is risk transfer. The transport company pays a premium so the insurer agrees to absorb specified losses under specified conditions. The key phrase is “under specified conditions.” A policy isn't a blanket promise. It's a contract with triggers, exclusions, and priorities.

Think of it this way:

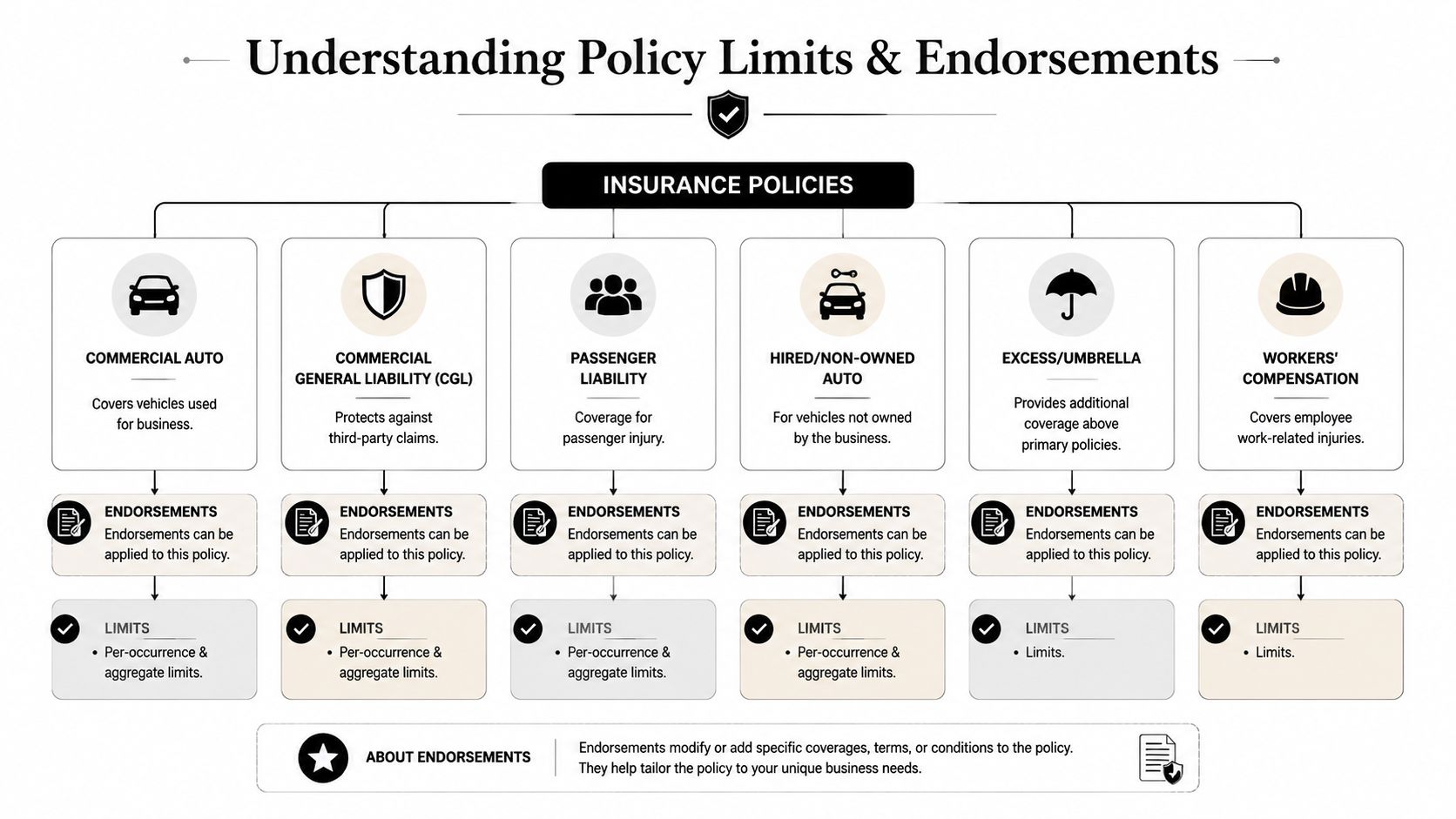

- Commercial auto covers the vehicle operation itself. If a chauffeur causes a road incident, this is often the first place people look.

- Commercial general liability, often called CGL, responds to third-party bodily injury or property damage claims that aren't strictly auto claims.

- Passenger liability matters because the people in the vehicle are the center of the service.

- Hired and non-owned auto becomes important when the company uses vehicles it doesn't own.

- Umbrella or excess liability adds another layer above certain primary policies.

- Workers' compensation addresses employee injuries tied to work.

Why each policy exists

A curbside slip during luggage handling may not be the same kind of claim as a collision. A substitute affiliate vehicle may not fit neatly under the same coverage logic as a company-owned sedan. A chauffeur injured while helping a client may trigger a different insurance response than a passenger injury claim.

That's why executive transport needs more than a single “auto policy confirmed” box on a vendor form.

The useful question isn't “Do you have insurance?” It's “Which policy responds to which part of this trip?”

Where readers usually get confused

Confusion tends to come from overlap. People assume overlapping means duplicate. It usually doesn't. Instead, each policy handles a different slice of the exposure.

A simple mapping helps:

| Exposure | Policy likely involved | Why it matters |

|---|---|---|

| Vehicle accident during client transfer | Commercial auto | Core driving-related claim |

| Client trips on steps at pickup site | CGL | Premises or operational liability |

| Affiliate sends replacement car | Hired/non-owned auto | Extends beyond owned fleet |

| Claim exceeds base policy | Umbrella or excess | Added protection above primary layers |

| Chauffeur injured while working | Workers' compensation | Employee injury response |

Once you see policies as separate tools rather than one big shield, insurance coverage details become easier to read and much harder to fake.

Policies Limits and Endorsements

A vendor sends over a certificate showing the right policy names and what looks like a healthy limit. An event planner signs off. Later, a claim involves an affiliate vehicle, and the hard question appears: did the policy extend to that setup, or did the protection stop at the named company and its owned cars?

That is the core work in this section. Limits tell you how much money may be available. Endorsements tell you when the policy responds, for whom, and in what order. For executive mobility professionals, that difference matters because trips are often arranged through booking entities, fulfilled by affiliates, and performed across more than one legal or geographic boundary.

Some public procurement standards for transportation vendors illustrate the point. One municipal framework sets higher liability benchmarks than many buyers expect, including per-occurrence and aggregate requirements for service providers in complex transport arrangements, as shown in this municipal insurance requirement exhibit. Use figures like that as a reference point, not as proof that every executive transport program is protected in the same way.

What limits answer, and what they do not

A policy limit answers one question: how much can this policy pay, subject to its terms? It does not answer whether the claim falls inside the policy, whether an affiliate arrangement is included, or whether your organization receives any direct protection.

That is where readers often get tripped up.

A simple way to read this is to treat limits like the size of a water tank and endorsements like the valves controlling where the water can flow. A large tank helps. A closed valve still leaves the fire burning.

For executive transport, start by checking whether the limit matches the exposure created by the trip. A single airport transfer for one traveler is different from a roadshow using multiple affiliates, high-profile passengers, and tight timing. The more moving parts involved, the more attention you should give to excess layers, hired and non-owned auto language, and contract-specific endorsements.

How the main policy layers work in practice

Commercial General Liability, often written on ISO form CG 00 01, usually addresses bodily injury, property damage, personal injury, and some operational exposures that are not tied directly to driving. If a client says the harm came from service operations outside the actual vehicle accident, CGL may be the policy that responds.

Commercial auto liability covers vehicle-related claims and should be reviewed for owned, hired, and non-owned exposure. That last part matters for executive mobility programs that book under one company name but fulfill through local partners. A provider can look well insured on paper while still leaving a gap if the actual vehicle was supplied by an affiliate and the policy language does not extend as expected.

Workers' compensation sits on a different track because it addresses employee injury obligations. It does not replace auto or general liability. It fills a separate function tied to the employer-worker relationship.

This is why executive mobility buyers should read policies as a stack of tools, not one blanket promise.

The endorsements that usually decide whether the program holds up

Three endorsements deserve close review because they change how a claim unfolds after the incident, not just how the certificate looks before it.

Additional insured language can extend liability protection to your company when claims arise out of the transport provider's operations. Without it, your organization may still get named in a lawsuit, but you may have less direct access to the vendor's liability coverage.

Primary and non-contributory wording affects priority. If your company also carries its own insurance, this endorsement can help make the transport provider's policy respond first instead of pushing your insurer into the first round of payment and defense allocation.

Waiver of subrogation affects what happens after an insurer pays. It can limit the insurer's ability to seek repayment from a contractual partner, which can matter when multiple companies touch the same trip.

For executive mobility professionals, the hidden issue is often not whether these endorsements exist in theory. The issue is whether they apply to the exact legal entity, affiliate chain, and service arrangement involved in the booking.

The underinsured gap that standard guides often miss

A provider may meet a stated minimum and still be underinsured for your real exposure.

Here is a common example. A booking company shows acceptable limits. The actual trip is fulfilled by a smaller affiliate in another city. That affiliate has lower limits, narrower hired and non-owned auto wording, or no endorsement extending protection to the contracting parties upstream. On paper, the program looked aligned. In the claim file, the protection is thinner than expected.

That gap is easy to miss because standard coverage guides often stop at “policy present” and “limit meets requirement.” Executive mobility programs need one more question: does the coverage structure stay intact when the trip moves from contracted provider to affiliate provider?

Contract language is where you close much of that gap. For teams documenting these expectations in advance, preferred vendor agreements for executive transport should spell out required limits, affiliate obligations, and endorsement language before any ride is dispatched.

A final caution. Endorsements can broaden coverage, but they can also narrow it. Read them the way an event planner reads a venue addendum. The headline may say the ballroom is included, but the attachment may in its fine print exclude loading access, after-hours staffing, or third-party vendors. Insurance endorsements work the same way. The details decide whether the plan works under pressure.

Reading and Verifying Certificates of Insurance

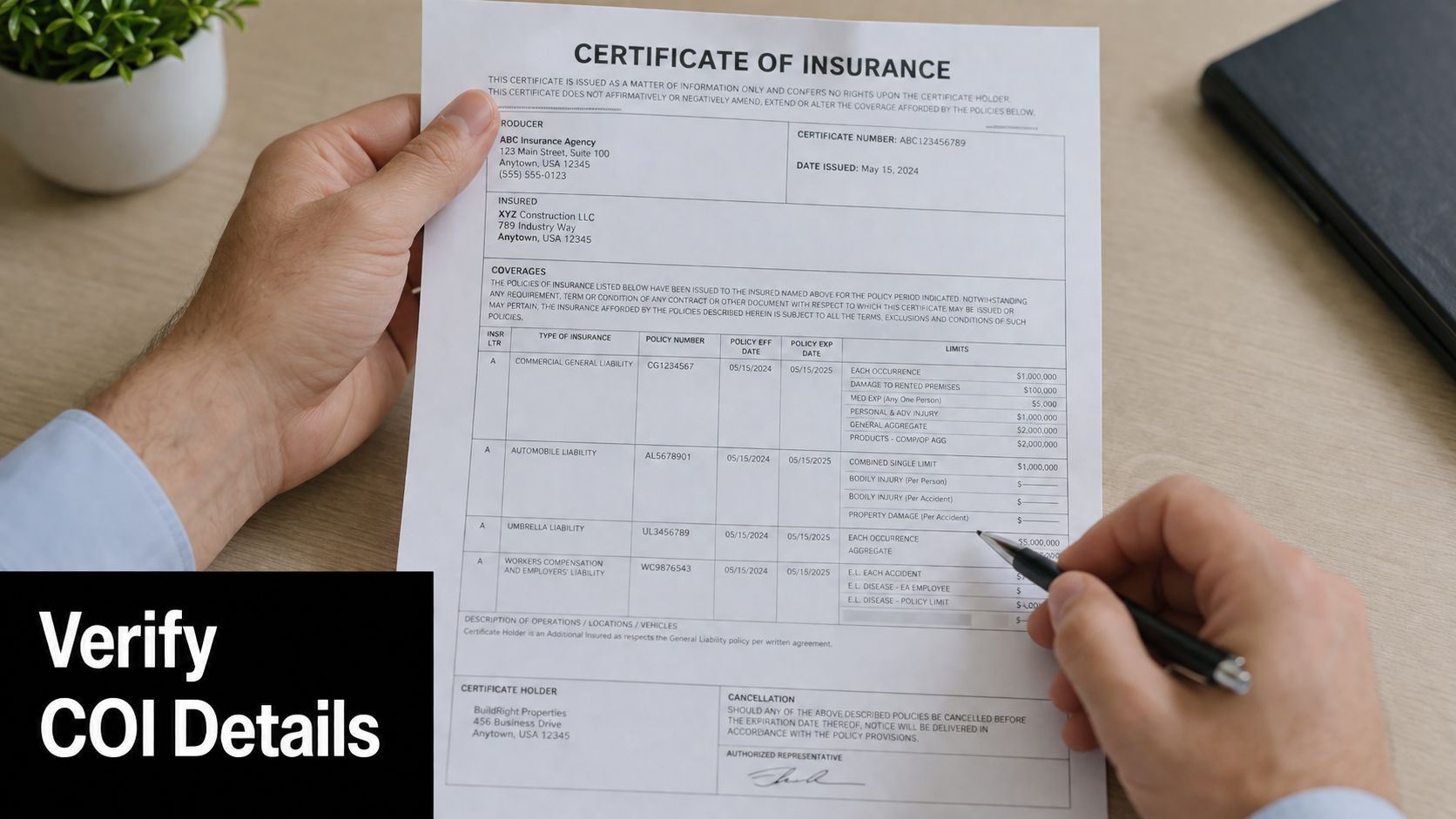

A certificate of insurance, or COI, is a snapshot. It's useful, but it isn't the policy. That distinction matters because many planners treat the certificate as final proof when it's really a summary with limits.

When you read a COI for executive transport, don't start with the limits. Start with the named insured. If the booking confirmation says one company and the COI names another, pause. It may be a parent company, a DBA, or an unrelated affiliate. You need that relationship explained in writing.

A simple COI reading sequence

Use this order every time:

Named insured

Confirm the legal entity on the COI matches the contracting party or clearly explains the relationship.Policy effective dates

The trip date must fall inside the active coverage period.Coverage lines

Look for commercial auto, CGL, workers' compensation, and any excess or umbrella listing that applies.Limits

Check whether the limits meet your internal requirement.Description box

This is often where additional insured language, waiver of subrogation, or project-specific wording appears.Certificate holder

Make sure your entity is listed correctly if required by contract.

What a red flag looks like

Here's the kind of excerpt that should trigger questions:

Named Insured: Executive Transport Holdings LLC

Description: Operations as per contract

Auto: Listed

CGL: Listed

Additional Insured: Not shown

Hired/Non-Owned: Not visible

That doesn't prove a problem, but it doesn't prove protection either. “Operations as per contract” is not the same thing as seeing the endorsement language itself. If the certificate says an endorsement applies, ask for the endorsement schedule or the policy form reference.

Readers often get tripped up by cancellation wording too. A COI may mention notice provisions in a general way, but the policy controls. If your event depends on continuing coverage, don't rely on assumptions about notice.

For a visual walk-through of how insurance documents are usually structured, this short explainer helps frame what you're looking at before you review one under deadline pressure.

Questions to ask when the COI is vague

- Who is operating the vehicle? The certificate may belong to the booking entity, not the service-delivery entity.

- Does hired and non-owned auto apply to affiliates? If that isn't clear, affiliate use can become a blind spot.

- Can you provide the endorsement form or schedule? This is the quickest way to move from assumption to verification.

- Does umbrella coverage sit over all relevant primary policies? Not every umbrella attaches to every exposure.

A COI should reduce uncertainty. If it creates more, treat that as a sign to slow down.

Claims Process and Jurisdictional Nuances

Claims handling feels straightforward until the trip crosses a border, involves a medical component, or pulls in multiple insurers. Then it starts to resemble customs clearance. The package exists, the paperwork exists, but nothing moves until the right authority gets the right file in the right format.

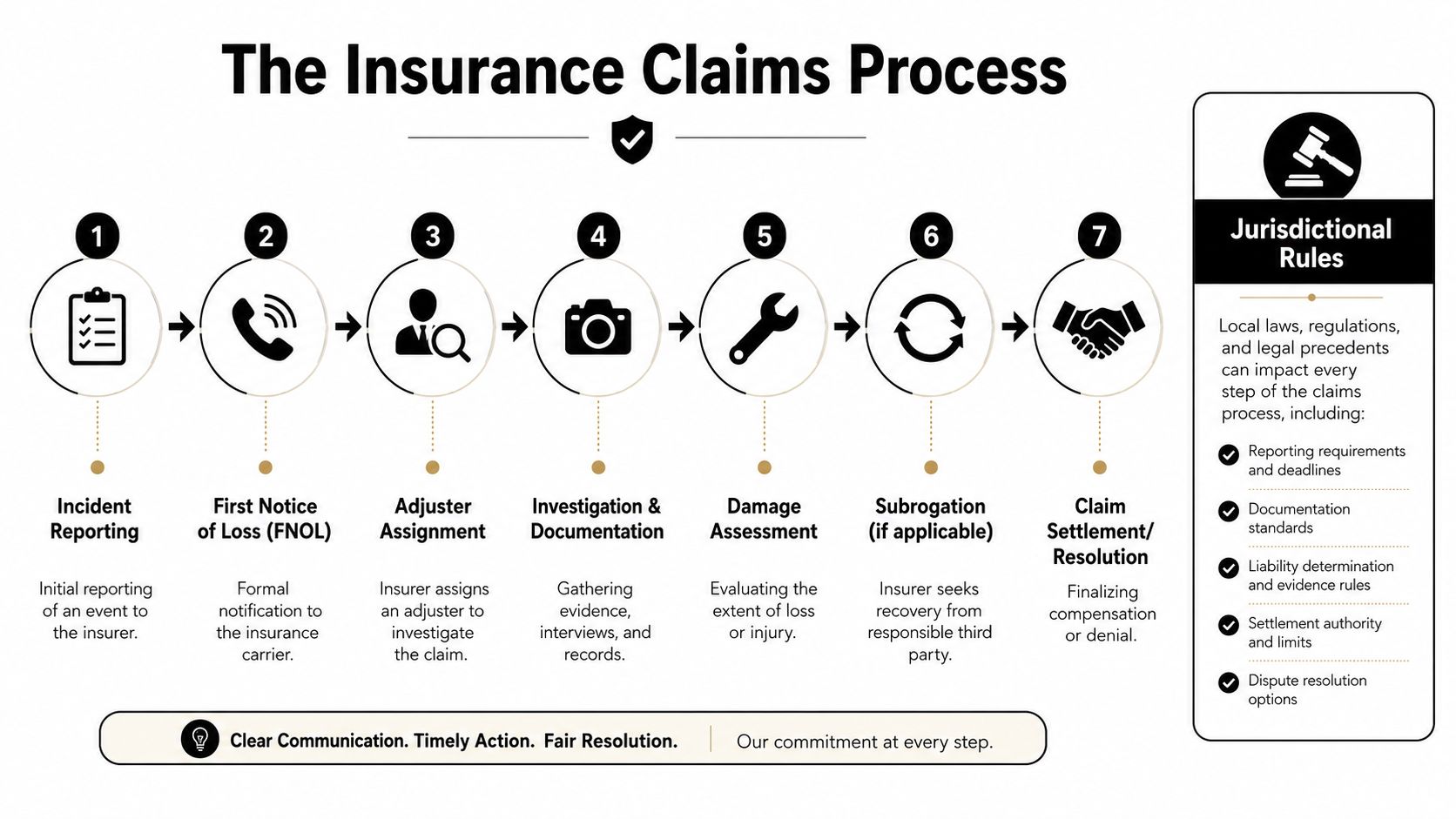

How the workflow usually unfolds

The basic sequence is familiar. Someone reports the incident. The carrier receives a first notice of loss. An adjuster gets assigned. Evidence, statements, and records are collected. Damages are evaluated. If another party may be responsible, subrogation may follow. Then the insurer resolves or denies the claim.

That sounds linear, but executive mobility adds complications. There may be a booking agency, a local affiliate, a venue, and the client's own risk team. Each may have separate reporting expectations. If one party delays notice, the claim file starts weak.

Why jurisdiction changes the experience

Local law can alter documentation, timing, driver reporting duties, and who pays first. One region may emphasize vehicle-based liability rules. Another may involve different treatment of bodily injury claims or recovery rights. If the trip runs across several countries, your operations team needs the incident facts preserved in a way that multiple insurers and legal systems can understand.

A broader travel risk framework helps here. It allows a corporate travel risk management guide for mobile executive programs to become operational, not theoretical.

If a claim could touch more than one country or more than one provider, collect documents as if a second reviewer will challenge every detail.

There's another modern wrinkle. In 2024 to 2025, 28% of coverage denials for non-emergency services were linked to AI-driven algorithms rather than human review, according to this discussion of insurance coverage experience and denial patterns. For mobility professionals coordinating medical support around executive travel, that means urgent appeals may need human escalation fast. A denial isn't always the end of the file. Sometimes it's the start of a procedural fight.

Verification Checklist and Questions for Providers

Most insurance reviews fail for a simple reason. People ask for documents, not answers. A provider can send a current COI and still leave major gaps untested.

Use a checklist that ties each document request to a practical question.

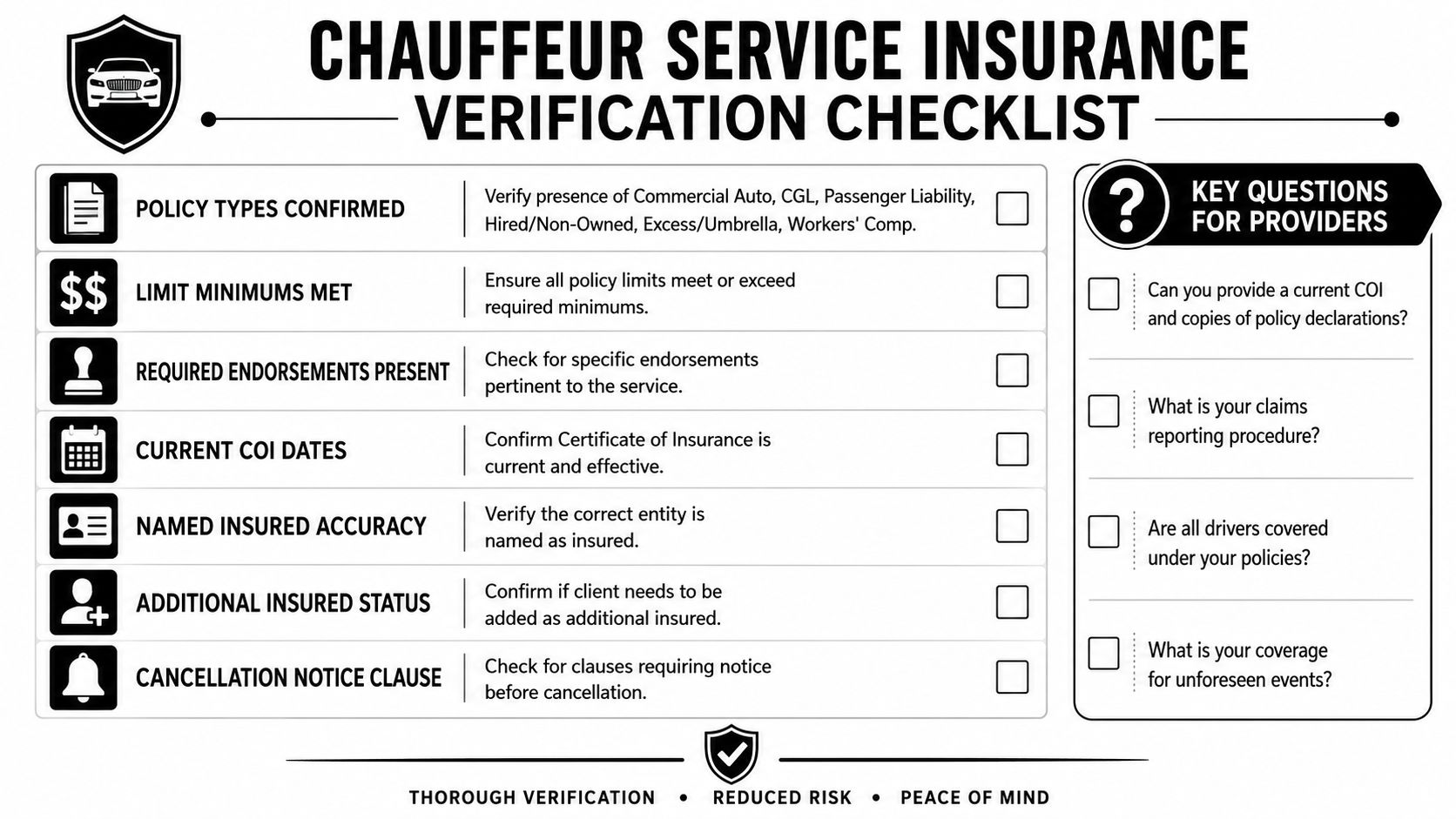

A working review list

Policy mix confirmed

Ask whether commercial auto, CGL, hired and non-owned auto, excess or umbrella, and workers' compensation all apply to the service model being used.Limits reviewed against your standard

Ask the provider to confirm not just the existence of limits, but which policy carries them and whether they apply to affiliates.Endorsements verified, not assumed

Request proof for additional insured status, primary and non-contributory wording, and waiver of subrogation when your contract requires them.COI dates checked

Confirm the coverage remains active for the service dates, including any extension, standby, or return segment.Named insured reconciled

If the entity on the COI differs from the operator name on the quote, ask for the legal relationship in writing.

Questions that uncover hidden gaps

Use direct language. For example:

| What to ask | Why it matters |

|---|---|

| Can you provide a current COI and copies of policy declarations? | The COI alone may not show enough detail |

| Are all drivers covered under your policies? | Driver classification issues can derail claims |

| What is your claims reporting procedure? | Delayed notice creates avoidable friction |

| What is your coverage for unforeseen events? | Tests how the provider thinks about non-routine incidents |

One gap many buyers miss sits outside fleet liability. In health and travel contexts, people may be underinsured even when they have coverage. The GoodRx explanation of underinsurance notes that out-of-pocket costs above 10% of household income can place someone in the underinsured category. For executive mobility professionals, that matters when trips involve medical escorts, emergency treatment coordination, or evacuation support. A COI can look clean while the traveler's broader protection still carries painful exposure.

For teams formalizing provider vetting, an executive chauffeur checklist for VIP travel approvals works best when insurance questions sit beside dispatch, vehicle, and security checks instead of living in a separate folder.

How MLR Worldwide Service Meets Best Practices

A flight lands early, the pickup location shifts to a private terminal, and the assigned vehicle has to be replaced. That is the kind of moment that tests whether a provider's insurance process works. For executive mobility professionals, a key question is not whether a file exists. It is whether the provider can show, in real time, that the right entity, vehicle, driver, and affiliate arrangement are still covered after the plan changes.

That standard matters because executive transport rarely stays inside a simple one-car, one-stop scenario. Roadshows, FBO transfers, security-driven reroutes, and last-minute affiliate substitutions create pressure points where hidden coverage gaps can appear. Endorsements matter here. So does the difference between a clean-looking certificate and the actual policy terms behind it. As noted earlier, buyers should compare a provider's program against the level of scrutiny commonly used in formal insurance requirement frameworks, without assuming a summary document answers every question.

MLR Worldwide Service aligns with that best-practice approach because its operating model depends on disciplined verification. The company coordinates executive chauffeur services, airport and FBO transfers, corporate roadshows, event logistics, VIP secure transport, and airline crew movements through a vetted global affiliate network. In practical terms, that means insurance review cannot sit in a folder untouched. It has to function like a pre-event run of show, with checks completed before the itinerary starts and escalation steps ready when details change.

The stronger signal is operational clarity.

A serious provider should be able to explain who reviews affiliate insurance, how endorsement requirements are tracked, what happens if a substitute vehicle is dispatched, and how incident reporting works after hours or across borders. That level of detail helps buyers spot a common blind spot in executive mobility. Coverage can appear adequate at the top line while a specific endorsement, named insured detail, or affiliate handoff creates a gap lower down.

For planners and mobility teams, that distinction is similar to venue planning. A ballroom may look perfect on the floor plan, but the event still fails if the loading dock, power access, and credential list were never confirmed. Insurance works the same way. The headline policy matters, but the handoffs matter too.

The best insurance file is the one that has already been checked before the itinerary changes.

Conclusion

Insurance coverage details matter most when the schedule gets messy. That's when missing endorsements, unclear insured names, and weak claims procedures stop being technical issues and start disrupting executive travel.

The practical approach is simple. Match policy types to real trip exposures. Read COIs in a fixed order. Verify endorsements instead of trusting summaries. Ask providers how affiliate vehicles, claims reporting, and priority of coverage work before the pickup. Watch for underinsured gaps when medical or travel protection enters the picture.

Event planners and travel managers already know how to pressure-test a timeline. Insurance deserves the same discipline. Once you review it that way, the documents become easier to read and the weak spots become easier to catch before they become your problem.

If you need a ground transportation partner that understands the operational side of risk, MLR Worldwide Service supports executive travel with global coordination, vetted chauffeur standards, and the kind of planning discipline that helps keep complex itineraries protected and on schedule.